HOW TO SET UP A FAMILY FOUNDATION

It’s as easy as setting up a bank account!

Like a precision timepiece, The American Foundation has a smooth running process that allows you to benefit from complicated tax laws by using our simple Donor Advised Family Foundation Program

Three Easy Steps:

1. Read this Donor Advised Family Foundation Program

2. Complete the Donor Application

For those who have questions about which assets would be most advantageous to be contributed, or would like The American Foundation to provide charitable planning suggestions and a custom illustrated proposal, please feel free to contact us.

3. Mail your check and signed application to:

The American Foundation

4518 North 32nd Street

Phoenix, AZ 85018

ESTABLISH YOUR LEGACY

Create Your Own Family Foundation

In the past, people have established wills that will give money directly to a charity at the time of their death. A better way is to create a family foundation while you are living to get the equivalent of a double or triple tax deduction, and, at the same time establishing a legacy of perpetual family giving.

Not only can you fund your Family Foundation with cash, real estate, securities, and business interests , but your Family Foundation can also be designated as the beneficiary of every kind of planned gift or charitable trust permissible under tax law. And most importantly, Family Foundations at The American Foundation™ receive the higher, public charity tax deductions.

Recognizing the meaningful support charitable foundations can provide to our nation’s communities, our tax laws offer significant benefits to anyone who contributes to a foundation. And perhaps the greatest benefit is the opportunity you will have to help a vast number of worthwhile charities.

The American Foundation helps individuals and families create Family Foundations that give perpetual financial support to their favorite charities. We do not provide tax advice, but we do help educate prospective donors about the tax and financial benefits that provide great incentives for individuals to be philanthropic. In many cases, these plans can actually help donors increase their income while also lowering their taxes. In addition, ancillary techniques readily available with the assistance of other tax and financial professionals, can help donors transfer more wealth to heirs tax free.

At The American Foundation, we want people to become personally involved with their family foundation and the charities they support. In fact, we believe the more and longer a donor is involved, the better. Three good things happen when individuals, families, and business leaders become more involved in the charitable process:

- they tend to give more,

- they become better people, and, in most cases,

- the charity or charitable programs they support become more

effective and successful.

Because of continued donor involvement, those who establish a Family Foundation account at The American Foundation acquire what we call Charitable Ownership.

HOW DOES A FAMILY FOUNDATION AT THE AMERICAN FOUNDATION WORK?

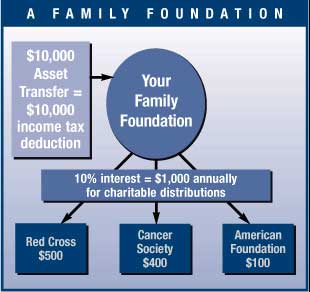

Setting up a family foundation at The American Foundation is easy! After filling out a simple Donor Application, cash or assets can be transferred into the donor’s family foundation account at The American Foundation (foundations are established with a minimum deposit of $100,000). Each foundation can carry the namesake of the donor family or any other name the donor chooses.

The funds in the family foundation are then managed for growth and income. At least 5% of the annual value of the foundation is distributed each year from income or growth to family-selected charities. Principal will be preserved. Any undistributed income or growth is added to principal, allowing the foundation to grow.

BENEFITS OF FAMILY FOUNDATION PLANNING

- Provides great asset protection

- Eliminates estate and gift tax

- Can significantly increase annual tax-advantaged personal income, through the use of our CRT Advantage™ Income Trust

- Generates income tax deductions

- Eliminates capital gains tax on the sale of appreciated stock and properties

- Provides annual support to family-selected charities

- Establishes a “family charitable legacy”

- Can provide increased inheritance to heirs when life insurance is used in a trust to replace the amounts gifted. We call this a Wealth Enhancement Trust™.

WHAT MAKES THE AMERICAN FOUNDATION SPECIAL?

We support donor involvement

The American Foundation offers a great amount of donor direction. Foundations established at The American Foundation carry the name of the donor, or whatever other name the donor wishes. Donors then have the ongoing opportunity to recommend where their charitable grants go, now and forever, continuing the donor’s charitable mission in perpetuity. We call this feature “Charitable Ownership.”

We are international in scope

Many people like to support charities in places other than where they are currently living, such as their hometown, or in some other area that is close to their heart, perhaps in other less fortunate parts of the world. The American Foundation is international in scope. Our donors can give to qualified charities and charitable programs anywhere in the world.

We help charities become more successful

Our organization was founded over twenty-five years ago by a few individuals dedicated to making the world a better place by helping charities to be more successful. We do this by creating more money for charity, helping charities to improve their operations, and building cooperation among charities to maximize their reach and effectiveness. By becoming a donor, you are participating in our charitable mission -promoting and facilitating the privatization of philanthropy™ which results in new and more effective philanthropy.

We Offer Great Opportunities

The American Foundation provides a donor with opportunities to:

- make charitable contributions of cash, property or securities to their family foundation;

- receive the maximum tax benefits associated with a gift to a public charity;

- increase the effectiveness of their philanthropy through the expert assistance of The American Foundation;

- recommend grants from their family foundation to qualified charitable organizations anywhere in the United States or the world;

- create a family foundation that becomes an ongoing family charitable legacy; and

- protect assets and diversify investments.

ABOUT THE AMERICAN FOUNDATION

The American Foundation is a 501(c)(3) public charity. We have the same status as most churches, youth organizations, and universities. We are a nonprofit organization and, as such, we have no “for-profit” element in our operations.

We achieve our charitable mission by helping individuals, families, and corporations create family and corporate foundation accounts that give financial support to their favorite charities. The American Foundation becomes one of the charities that the family foundation supports, but only at the nominal amount of 1% of foundation or trust account values per year.

The annual gift allocation to The American Foundation first pays for the actual cost of foundation account or trust administration. Remaining money is used to develop and expand our charitable mission of promoting and facilitating the privatization of philanthropy™ .

We strive to make the entire process of philanthropy easy and rewarding by providing simple procedures, ongoing education and the opportunity for increased donor involvement.

Our Mission

Our mission is to energetically promote and facilitate the privatization of philanthropy. We accomplish this mission in three ways.

- First, we help individuals, families and corporations establish charitable trusts and foundation accounts under unique and greatly improved operating formats.

- Second, we help foundations and other charities become more efficient and successful in their operations.

- Third, we build networks of cooperation, mutual assistance, and support among charities, foundations, and donors to accelerate good in the world.

How We Empower Our Vision

Philanthropy has been around as long as there have been people in need. However, the philanthropic community has not kept pace with new and innovative developments adopted by successful for-profit corporations. While tax laws and the global economy have been changing with dizzying speed, the structure and operation of most foundations and charities have not been altered significantly in more than a century.

The American Foundation works with individuals, families, corporations, communities, and professional tax advisers to establish charitable foundations and gift plans of all kinds. One of our goals is to revolutionize the structure, governance, and operations of charities and foundations. With better guidance and direction, charities and foundations can greatly accelerate their good works. Our growing American Family of Foundations offers the complete spectrum of exciting ways to maximize the social, tax, and financial benefits of charitable giving.

Governance and Organization (Structure)

We believe the control and direction of charities and foundations most appropriately belong in the hands of those who make it happen. We have developed organizational structures that put a great amount of direction in the hands of donors who fund foundation accounts and the visionaries who create charities. This proper structure can also ensure that successors are those who demonstrate a loyalty to, or a bonding with, the organization’s original vision and mission. Policies can be established that also ensure greater direction and cooperation among governing bodies, while eliminating most of the inherent problems that have historically plagued the “Board of Directors” or “Multiple Trustee” style of governance.

Operations

Most charities operate with hand-me-down equipment and facilities. Many charities go out of business because they are not operated like most competent and efficiently run for-profit businesses. Also, inefficient operations usually do not attract donations from the general public. No one wants to donate to a charity when there is a high risk of the charity losing money through mismanagement, excessive overhead, or inadequate facilities and equipment. Access to high technology and leading edge equipment and procedures will help any operation become more successful. The American Foundation advocates increased grant making and financial support to operating charities that need assistance in this area. Under our program, those who work with charities can receive assistance and training in business management, computer use, marketing techniques, and other areas that will help them be more efficient and effective.

Human Resources

The success of any operation is directly related to the skill level and expertise of its staff. This valuable resource is often neglected in charities. When highly competent individuals become highly motivated in a worthwhile endeavor, an empowerment develops that leads to extraordinary success. We encourage all charities and foundations to increase their efforts to identify, recruit, and hire the most outstanding people available. Good leaders are the geese that lay golden eggs. Instead of funding grants for charitable programs that struggle because of inefficient leadership, The American Foundation believes that grant makers should direct more funds to stimulate and enhance “charitable production capacity.” Finding exceptional leaders and workers, and attracting them to the field of philanthropy is critical to the success of what is arguably the most important endeavor of mankind.

WHAT WE CAN DO FOR YOU

At The American Foundation, our knowledgeable staff is dedicated to creating the most beneficial scenario for both donors and charities. We want to make the entire process enjoyable and simple by offering the following benefits and services free of charge:

1) Our Charitable Giving Program

We help with the preparation, review, and implementation of all types of charitable trusts and other major gift plans that can fund your family foundation. We handle the details, making the process easier for you, by:

- Working closely with you and/or your professional tax advisers to ensure compliance with IRS guidelines;

- Providing on-going charitable gift-related tax information;

- Accepting many different types of assets for gifting purposes, including cash, stocks, real estate, business interests and other properties;

- Assisting with the suggested design of trusts and family foundations tailored to a person’s unique needs and objectives;

- Providing compliant foundation documents for all gift plans and charitable trusts.

2) Charitable Grants

We process all charitable grants:

- Review and verify the charitable status of recipient charities;

- Assist in the calculation and issuance of grants to charities.

3) Investments/Charitable Account Management

Our goal is to achieve above average rates of growth and/or income on foundation assets and charitable accounts. To that end, we:

- Implement sound investment strategies using what is called the Investment Advantage™approach;

- Monitor investment activity for compliance with IRS regulations and trust document guidelines;

- Implement other innovative programs that achieve growth and/or income to foundation assets and charitable accounts.

4) Education and Reporting

We provide:

- Annual reports on trust and foundation performance;

- Periodic reports as may be requested by a donor.

5) Accounting and Taxes

Our accounting department:

- Issues a gift receipt to donors;

- Calculates the appropriate charitable grants and income distributions from trusts and family foundation accounts;

- Will assist selected CPAs with the preparation of foundation audits and/or trust tax returns.

Become a Member of The American Family of Foundations

The American Foundation is developing an expanded national network of foundations that we call The American Family of Foundations. With this network of family, community, corporate, and international foundations, we help member foundations cooperate with one another and correlate their efforts, resulting in more effective philanthropy. We understand the value of working together for the common good of our society.

Just as “families” of mutual funds give investors an opportunity to accomplish many different investment goals within an extended group of funds, our family of foundations offers every opportunity imaginable for improved charity and philanthropy.

FAMILY FOUNDATION FORMAT DESCRIPTIONS

Structured to Suit Your Needs

A family foundation may be established in any of the following forms or structures:

- A component family foundation charitable account at The American Foundation™,

- A stand-alone support organization, or

- A stand-alone private foundation.

The experienced staff at The American Foundation can work with you and/or your professional tax advisers to help you determine which type of family foundation account is best for you.

Format Descriptions

Component Family Foundations

(A component charitable foundation account at The American Foundation).

This type of foundation is highly preferred for all foundations regardless of size. A family foundation is a charitable account created to provide ongoing financial support to donor recommended charities. Assets donated to The American Foundation for a family foundation are managed to achieve income and/or growth, and then all or part of the annual income or growth is distributed to family selected charities. This is the simplest and easiest family foundation format to operate. Cash or assets are transferred directly to The American Foundation for the particular family foundation account of the donor establishing the fund. This foundation is established with a minimum deposit of $100,000.

The American Foundation is a qualified 501(c)(3) public charity. All of its family foundation component accounts qualify for the same public charity tax status. Donors qualify for the highest tax deductions – up to 50% of AGI for contributions of cash and 30% of AGI for donations of appreciated properties. Excess deductions can be carried forward for five years. The assets are managed for income and growth. The donor or the donor’s designee makes recommendations for grants of all or part of the annual income and growth to qualified public charities.

Unless specifically noted otherwise, all donations accompanying an application will establish this preferred and standard component family foundation with The American Foundation.

Support Organization

A support organization is a foundation formed to support a particular charity or cause. A support organization is an entirely separate entity with its own 501(c)(3) tax status.

The American Foundation has pioneered the use of support organizations as family foundations. A family foundation affiliated with The American Foundation, can provide special benefits.

This type of foundation is a public charity, so donors receive the highest tax deductions – up to 50% of AGI for contributions of cash, and 30% of AGI for donations of appreciated property. Excess deductions can be carried forward for five years. The support organization format is well suited for very large foundations where the donor wants continued hands-on administrative involvement. It can be set up as a trust or a corporation, depending on its size and nature. The American Foundation will help you determine which format is best for your situation.

The donor or selected family members can be appointed as trustees or board members. Special procedures are implemented in the governing documents and by-laws to ensure continued adherence to the donor’s charitable mission and objectives. This type of foundation may raise money as an independent entity, apply for grants, and have its own offices, officers, employees, and programs.

Private Foundation

By and large, this approach has fallen out of favor with most tax and foundation planners because of the reduced tax benefits and burdensome regulations. However, The American Foundation can “adopt,” convert, and/or administer existing private foundations, bringing them into its extended Family of Foundations’ operations. And, there are some circumstances that warrant the creation of private foundations that work in tandem, or in concert, with our family foundations at The American Foundation.

This foundation type is a totally separate and distinct entity. In addition to having increased responsibilities and liabilities, there are many tax and administrative disadvantages. There are also other restrictions and limitations that prevent the donor from achieving many tax and financial objectives that can otherwise be achieved with a family foundation under our public charity format. Deductions for gifts of cash are limited to 30% of Adjusted Gross Income, 20% for donations of appreciated property.

The American Foundation is well suited to assist you in the administration of a private foundation. A private foundation can be best utilized in conjunction with one of our public charity foundation formats. The synergistic benefit of being part of The American Family of Foundations is much better than acting alone.

GIFT PLANS:HOW TO FUND YOUR FAMILY FOUNDATION

A family foundation charitable account can be funded with cash, stock, real estate, or other assets. Assets can also be placed into any number of special gift plans or trusts that will later transfer into a family foundation.

Outright Gifts

If you want your gifting to be more personalized and if you want to be more involved with your philanthropy on an ongoing basis, you are much better served gifting to your own family foundation at The American Foundation™. A cash donation is the easiest and most direct way to start a family foundation. Cash, stock, real estate, and other assets can be gifted to The American Foundation and then transferred directly into a family foundation account. This achieves the maximum tax advantages for the donor while providing continuing charitable involvement. Most people don’t fully realize the double, and sometimes triple, deduction benefit of a lifetime gift. Making a charitable gift while you are living gives you both a current income tax deduction and an estate tax deduction. And In some cases, you can also get the equivalent of a third deduction by avoiding capital gains taxes.

Gifts of Cash – If you itemize, you can lower your income taxes simply by writing a check to The American Foundation which then goes into the family foundation charitable account. If your name is John Smith, all you need to do is simply write a check to The American Foundation with a note on the message line for “The John Smith Foundation”. You can start a family foundation with a minimum deposit of $100,000. Gifts of cash are fully deductible-up to a maximum of 50% of your adjusted gross income. For example, if your adjusted gross income for this year is $300,000, up to $100,000 of cash gifts may be deducted this year. Any excess deductions can generally be carried forward and used over as many as five subsequent years. Anything that you move from a personal or living trust to a family foundation essentially transfers assets from a taxable account to a non-taxable account.

Gifts of Stock – It is often more tax-wise to contribute stock than cash into your family foundation. Gifts of appreciated stock can offer the equivalent of a triple tax deduction. First, you receive an income tax deduction for the full fair market value of the stock at the time of the gift (if held for over one year). Second, you avoid paying any capital gains tax when your family foundation sells the stock. And third, the stock is removed from your estate, which is equal to a full estate tax deduction. Gifts of appreciated stock are 100% income tax deductible — usable up to 30% of your adjusted gross income for the first year with the balance deduction carried forward for five additional years.

Gifts of Real Estate and Business Interests – A gift of real estate or business interests to your family foundation can also be tax-wise. Similar to a gift of appreciated stock, real estate and business interests also offer the above-described three-fold tax savings. First, you receive an income tax deduction for the full fair market value of the real estate at the time of the gift. Second, you avoid paying any capital gains tax when your family foundation sells the real estate. And third, you reduce your estate and save estate taxes.

Gifts of Life Insurance – A gift of life insurance can provide a significant charitable deduction. You could purchase a new policy or donate a policy that you currently own but no longer need. To receive a deduction, designate your family foundation as both the owner and beneficiary of the life insurance policy. Check with our office or your insurance agent for more details.

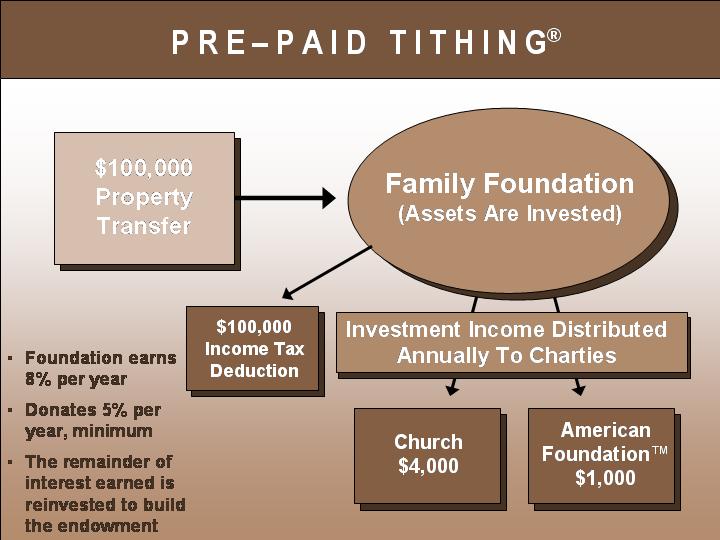

GIFT PLANS: PRE-PAID GIFTING (TITHING)

Many people make annual cash donations to their church. This practice is sometimes called payment of tithes.

We have developed a Gift Plan known as Pre-paid Tithing™ that achieves the equivalent of a triple tax deduction plus a life annuity. A Pre-paid Tithing plan can be established to support your church, religious organization, or other charity in perpetuity. The following example illustrates this planning technique.

- Step 1: An individual or family establishes a family foundation with The American Foundation™.

- Step 2: Real estate, stock or any other highly appreciated assets valued at $100,000 are transferred to your family foundation at The American Foundation.

- Step 3: The asset is sold and the proceeds invested – in our example we are assuming an 8% annual return.

- Step 4: Each year the family foundation distributes 5% to the family selected charities (donor’s church, etc.). In the above example, the assumed investment return is 8%, but only 5% is being paid out to charities each year, which allows the foundation account to grow by 3% annually. This would provide an ever increasing amount above the original $5,000 (5% of $100,000) that would be distributed to charities each year.

The donor achieves the equivalent of a triple deduction, plus a life annuity:

1. The donor receives a full $100,000 charitable gift income tax deduction, limited to 30% of AGI (50% if a cash contribution) in each year. Any unused deduction can be carried forward for five additional years.

2. Because The American Foundation is tax-exempt, there is no capital gains tax when the property or stock is sold. This is equivalent to an additional full tax deduction.

3. The property or asset is removed from the donor’s estate, which is equivalent to a 100% estate tax deduction.

4. Assuming that the donor in this case is normally making cash donations to his or her church or charity, the result of this new foundation account would be increased annual cash flow to the donor by the amount that he/she is no longer contributing personally to charity. The family foundation makes these same donations. This results in an increase in personal cash-flow for life, which is the definition of an annuity.

This plan works equally well with cash or assets that are not appreciated.

GIFT PLANS: CHARITABLE TRUSTS -A SPECIAL WAY TO FUND A FAMILY FOUNDATION

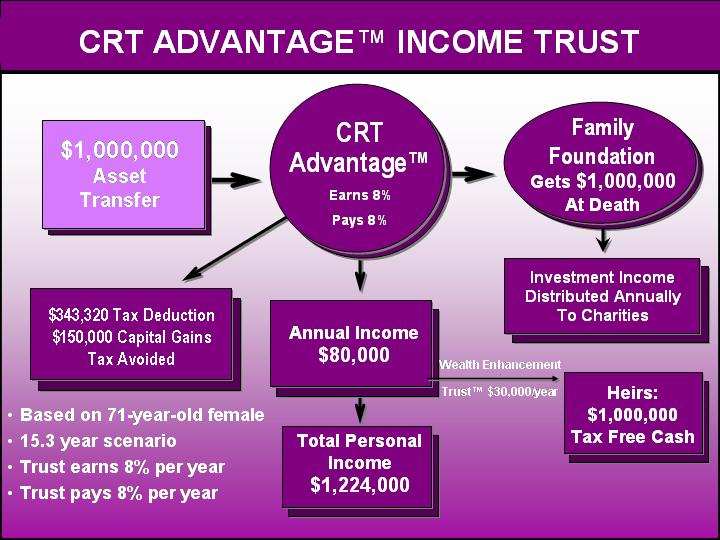

The CRT Advantage™ is an excellent tool for couples and individuals with highly appreciated or low income-yielding assets, who want or need additional income for life. The trust works quite simply. You transfer money, stock, or other property* to your CRT Advantage. This trust is tax-exempt, so when property sells, there is no capital gains tax. Sale proceeds are managed or reinvested for growth and income. The trust then pays one or more income beneficiaries (usually donor and spouse) an annual income for life. The “advantage” over traditional charitable remainder trusts is that the “remainder interest” after the donors’ lifetimes goes directly to The American Foundation™ for your family foundation– creating a perpetual charitable account that provides ongoing benefits to your family selected charities. This is why we call it the CRT Advantage.

The life-time income stream can be a fixed dollar payout (Annuity Trust) or a fixed percentage payout (Unitrust). After the lifetime income payments have been made, the trust transfers whatever amount is left to the family foundation.

Benefits of a Charitable Trust:

- The plan provides excellent asset protection for the donor and his or her family.

- The trust creates an opportunity to increase diversification of investments.

- The CRT Advantage is used in conjunction with a family foundation at The American Foundation

- Investments within the CRT Advantage have an advantage. We use an investment method called the Investment Advantage™. This method is designed to achieve higher fixed income returns.*NOTE: There can be no express or implied agreement to sell the asset prior to transferring it to the CRT. The property must be transferred to the charitable remainder trust before there is any contract in order for the donor to receive an income tax deduction and not have to pay any capital gains tax when the asset is sold.

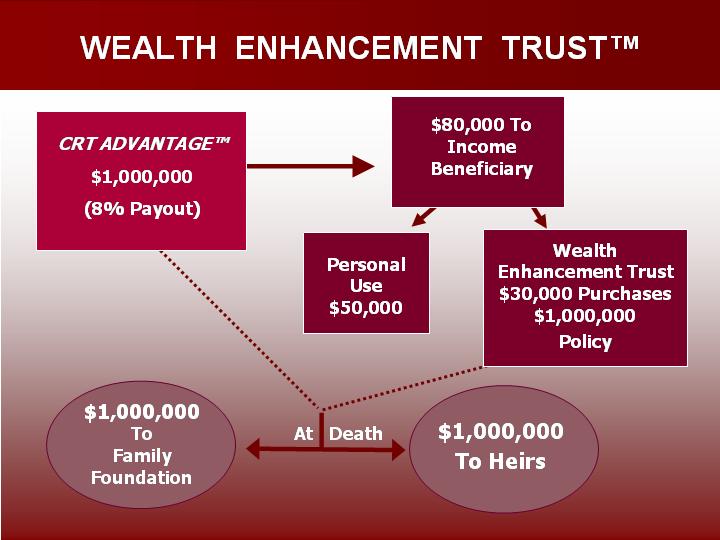

WEALTH ENHANCEMENT TRUST

A Wealth Enhancement Trust™ is an optional part of the family foundation process. This trust can assure that heirs are not “disinherited”. It is usually established in tandem with a CRT Advantage™ income trust or family foundation.

In the example, $1,000,000 in appreciated property is transferred to the CRT Advantage income trust. The trust is set up to pay 8% annually ($80,000 the first year) of the trust assets to the income beneficiary (usually donor or donor and spouse).

In conjunction with the CRT Advantage, a Wealth Enhancement Trust is also established. This trust is funded with a specially designed $1,000,000 life insurance policy. The money to pay the premiums for this policy come mostly from tax savings, and if tax saving are not enough then a small amount of the premium payments can come from the newly created increased income stream generated by the CRT Advantage.

At the death of the income beneficiary, $1,000,000 flows from the CRT Advantage trust into the donors family foundation. This creates a perpetual charitable family legacy. In addition, another $1,000,000 is paid to heirs tax-free.

When property is transferred to a charitable source such as a family foundation account or the CRT Advantage trust, that particular property is no longer owned by the donor, so it is not subject to estate tax. However heirs cannot receive property that has been used to create philanthropy.

The most tax efficient solution to this potential problem is to establish a Wealth Enhancement Trust. This is an irrevocable trust that is funded with a life insurance policy usually up to an amount equal to the value of the property transferred to your family foundation account or CRT Advantage trust. Because the policy is owned by an irrevocable life insurance trust (ILIT) and not by you, all proceeds will be paid to your heirs without incurring any income tax or estate tax.

This results in your heirs receiving one hundred percent of the value of the property that was transferred to the charitable entity. No one is disinherited from their inheritance. The donor, the heirs, and charities all win when a family foundation or CRT Advantage is coupled with a Wealth Enhancement Trust.

● You receive an income tax deduction

● You reduce or eliminate any estate tax

● You eliminate capital gains tax if using the CRTAdvantage

● Your heirs receive their full inheritance (and it is not subject to income tax or estate tax)

● Charities that you support will benefit from your philanthropy in perpetuity

Other names used for the Wealth Enhancement Trust are “Asset Replacement Trust” and “Wealth Replacement Trust”.

Any such Wealth Enhancement Trust planning is done outside and independent of The American Foundation. This information is included because it helps make philanthropy more attractive.

Please Note: If you or your attorney or CPA have any questions regarding any of our charitable planning concepts, The American Foundation™ is always available to answer any questions or explain any concepts.

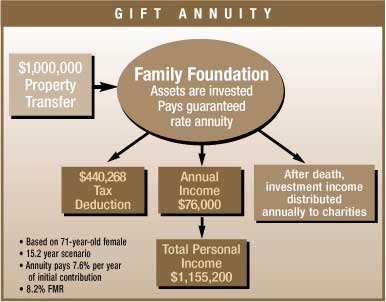

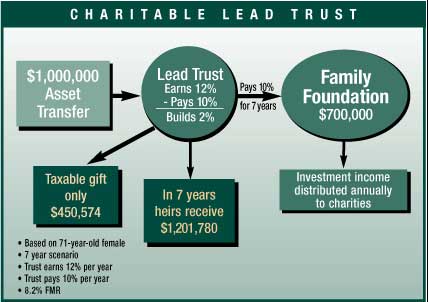

GIFT PLANS: GIFT ANNUITY AND LEAD TRUSTS

Gift Annuity (Immediate or Deferred)

The Gift Annuity is most attractive to those who want a steady stream of income for the rest of their lives while contributing to their family foundation. The American Foundation™ will pay a guaranteed fixed income for life-in return for charitable contributions of cash or property.

If you are married, your spouse can also be guaranteed the same fixed income for the balance of his or her life. The rate of return you receive depends upon your age (and, if applicable, the age of your spouse) at the time of your gift. The older you are, the higher the rate of return. You can be assured of receiving the same annual income from us – on a quarterly or other periodic basis – no matter what happens to the stock market or interest rates. And, a sizeable portion of each income payment from us will be tax-free. When you create a charitable gift annuity, you also receive a significant income tax charitable contribution deduction. There are also capital gains advantages if you fund the annuity with appreciated stock.

A lead trust is most appropriate for those in high estate-tax brackets who want to get appreciating assets out of their estate and eventually to their heirs without tax on the growth. The donor irrevocably transfers assets to a trust; the trust provides payments to his or her family foundation at The American Foundation™ for life or a term of years; then the trust principal goes to children, grandchildren, or others absolutely free of – or at greatly reduced-federal gift and estate taxes. Charitable lead trusts can be structured in three ways: (1) as a charitable lead unitrust which pays a specified amount annually to a family foundation; (2) as a charitable lead annuity trust which pays a guaranteed annuity annually to a family foundation; or (3) as a non-statutory charitable lead trust which pays all of the trust’s income annually to a family foundation. Further, charitable lead unitrusts and annuity trusts are sometimes created as “grantor trusts” to qualify the donor for the charitable income tax deduction. These trusts need not be grantor trusts to qualify the donor for the charitable estate tax deduction.

OTHER TYPES OF PLANNED GIFTS

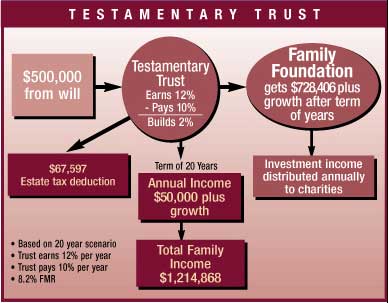

This gift plan can be placed in a testamentary plan as provided in a living trust document, will, or other testamentary device.

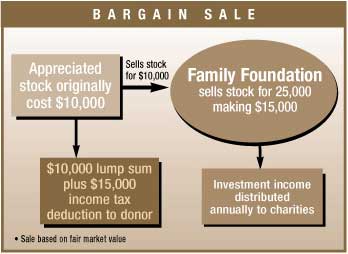

Those holding property not perceived to be readily marketable and who want an immediate cash return can receive an income tax deduction for the portion of the property contributed to a family foundation account. A bargain sale occurs when a donor sells appreciated securities (or other property) to his/her family foundation for less than present fair market value, intending to make a gift of the difference. A deduction is allowed for the difference between the property’s fair market value and the reduced sale price.

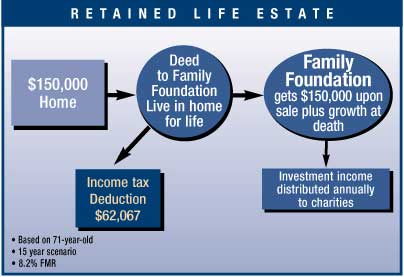

Many people plan to leave their homes to a charity in their wills. Naturally, they can’t make those gifts now because they need their homes. You can now leave your home or farm to your own family foundation account and retain the right to live there for your life (the life of your surviving spouse or other person can also be added). You get a sizable current charitable income tax deduction. The tax deduction is taken the year the property is donated based on the appraised amount and may be carried over for five additional years. The amount of your tax savings depends on your age and the value of your home. A gift of your home now, with retained life residency for you, gives you the same estate tax benefit as a gift by will. In addition, you save probate costs and receive an estate tax deduction. Similar tax benefits are allowed for a gift of your farm, and you retain the right to use the farm for your life (and to have a survivor use it for life, if you like).

Policies, Guidelines and Program Descriptions |

|

|

|

Introduction |

|

|

Donors and Contributions |

|

|

Family Foundation Management |

|

|

Grants to Charities |

|

|

Gift Allocation to The American Foundation™ |

|

|

Mission Integrity Policy |

|

|

Tax Considerations |

|

|

Record Keeping and Foundation Reporting |

|

|

Miscellaneous |

| Introduction | |

The American Foundation™ is a 501(c)(3) public charity. We create charitable accounts at The American Foundation (that we also call family foundations) that give financial support to a donor’s favorite charities. We strive to make the entire process of philanthropy easy and rewarding for the donor, by providing simple procedures, ongoing education and a great amount of donor direction for annual charitable grants. Contributions made to your family foundation established at The American Foundation are deductible at the highest “public charity” level. As with any charitable donation, the gift or transfer is complete and non-refundable.

Donors and Contributions

Eligible Donors

The American Foundation will accept contributions from individuals, companies, trusts, grant-making foundations, associations, and estates.

Donor Contributions

Contributions of cash, mutual fund shares, stocks, bonds, and other securities, including certain private and restricted stock, are eligible for contribution toa family foundation. Gifts to The American Foundation™ for its Donor Advised Family Foundation Program are not endowments, or endowment funds, even though they may have certain endowment-like traits. These gifts likewise are not gifts into trust but rather they are gifts to The American Foundation. The American Foundation represents that it will use its best efforts to always support and protect the integrity and viability of The American Foundation and its charitable programs, including its Donor Advised Family Foundation Program. The minimum initial contribution to establish a standard family foundation at The American Foundation is only $5,000. The minimum to create a charitable remainder trust is $250,000. Subject to approval, multiple donors may pool their contributions into a single foundation at The American Foundation. The minimum amount for additional contributions to an already existing foundation is $1,000.

All original contributions for a new foundation must be accompanied by a completed Donor Application, which can be delivered to The American Foundation via mail or facsimile. Cash contributions must be denominated in U.S. dollars and delivered by check or wire. Checks should be delivered to: The American Foundation, 4518 North 32nd Street, Phoenix, AZ 85018.

Review and Approval

All contributions are subject to review and approval by the Directors. Contributions not accepted will be returned as soon as is practical. The American Foundation will provide written confirmation at the time of acceptance of any contribution. The confirmation will include the amount of the contribution of any mutual funds or publicly tradable stocks, bonds and other property. The American Foundation does not value private securities, real estate or limited partnership interests. Donors should obtain an independent appraisal prior to making such a contribution for tax deduction purposes.

All contributions, once accepted by the Directors, represent irrevocable, complete and unrestricted charitable gifts to The American Foundation that are placed into family foundations under its Donor Advised Family Foundation Program. This is a Donor Advised Family Foundation Program donation and not a gift to an endowment fund or trust.

Accounts

The American Foundation will set up a component family foundation account, which will be used to maintain an internal accounting of donor contributions and grants to qualified charitable organizations. Your contribution may be allocated to one or more investment accounts or otherwise managed to achieve growth or income. Contributions to component family foundation accounts may be placed in common accounts. Funds placed in common accounts will maintain the appropriate family foundation accounting, reflecting contributions, the foundation’s share of growth or income, and grant activity.

Securities

The American Foundation will determine in its sole discretion whether to hold or sell donated securities. If securities are sold, The American Foundation™ tries to obtain the most favorable sales price under the prevailing market conditions. For non-publicly traded securities, or other securities for which no readily liquid market exists, The American Foundation will exercise discretion as to the time and price of sales in an attempt to maximize the sales proceeds. Any costs incurred by The American Foundation necessary for the disposition of such securities (e.g., legal or appraisal fees) will be assessed to the family foundation account.

Under IRS rules and regulations, the fair market value of publicly traded securities is the mean of the high and low sales prices on the contribution date. Other rules apply if there were no sales on that date or if the securities are not publicly traded. In any event, the value of the deduction for contributed securities may differ from the actual sales price. The value of the contribution is determined on the date on which The American Foundation receives the asset. Therefore, the net proceeds from the sale of securities, and the corresponding value of the foundation, may differ from the charitable deduction attributable to the contribution.

Grants to Charities

Recommendations Of Grants

Donors have the right to recommend grant recipients. A “grant” is a gift from a foundation account, out of income or growth, to a recognized 501(c)(3), 509(a) (1) or 509(a)(2) public charity by way of the Grant Recommendation Form. The donor may also designate long term or ongoing recommended grants to named charities on the Donor Charitable Interest Worksheet. Any such recommendations are subject to review and approval by the Directors and/or The American Foundation staff as may be designated by the Directors. If the recommendations are approved, The American Foundation will then make the appropriate grants. If The American Foundation does not accept a recommendation, or if a recommended organization no longer qualifies as a 501(c)(3), 509(a)(1) or 509(a)(2) public charity at the time the grant is to be made, The American Foundation will make reasonable efforts to notify the donor and obtain recommendations for grants to alternative charitable organizations.

A Perpetual Charitable Account Which Can Grow

Family Foundations established at The American Foundation will be held as perpetual charitable accounts. Our goal and objective is to preserve principal which is then managed for growth and/or income. Part or all of the annual income or growth is distributed annually to qualified charities or charitable programs as may be recommended by the donor. Family foundations are expected to distribute 5% of the annual value of the family foundation each year. Annual interest or growth over 5% is added back onto principal allowing the foundation to grow. The American Foundation will notify family members, before the end of each year, the calculated 5% amount available for making annual grants.

Charitable Advisor Election

During his or her lifetime, a donor may designate and authorize in writing another person or group of persons (called the “charitable advisor(s)” or “Director(s)”) to recommend grants to charitable organizations. Once so authorized by a donor, those so designated shall possess the right to recommend grants at any time from the family foundation until written revocation of such right is actually received by The American Foundation from the donor.

Successor Charitable Advisor

Upon the donor’s death, the successor charitable advisor(s) shall be assigned the rights and duties associated with the family foundation account at The American Foundation. If a family foundation is maintained jointly, upon the death of one donor, the remaining donor(s), unless otherwise specified, would succeed to the rights to recommend grants to charities and designate successors. Successor Charitable Advisors would be engaged only at the recommendation of the donor(s) or after the deaths of all donors of the family foundation unless otherwise specified in writing.

The successor must provide written notification and sufficient proof to the Trustees of the donor’s death and will then succeed to all rights and duties of a donor to The American Foundation, including the ability to recommend subsequent grants. If the successor to this right is a minor, the Directors may require that the minor’s legal guardian make recommendations for grants. Successor individuals may in turn assign successors in the event of the successor individual’s death.

Grants to Public Charities

Grants can only be made to charitable organizations which are tax-exempt under Code Section 501(c)(3) and which are also public charities under Code Section 509(a) (1) or (2), or for qualifying charitable programs or projects as approved by the Directors of The American Foundation. Grants cannot be made to private foundations.

Grants to Foreign Charitable Organizations

The American Foundation will consider grants to foreign charitable organizations where we can properly monitor expenditure of those funds. The American Foundation may also make grants to charities that are qualified as Section 501(c)(3) public charities that in turn fund and exercise expenditure responsibility over foreign charitable activities.

Other Restrictions on Grants

Grants from The American Foundation may not be used in whole or in part for any pre-existing pledge or any private benefit (such as school tuition or scholarships that directly benefit a specific individual), dues, membership fees, benefit tickets, or goods bought at charitable auctions; nor may grants be used or lobbying, political contributions, or to support political campaign activities. The American Foundation will reject grant recommendations for improper purposes and will take remedial action if we discover that grants have been made for improper purposes, which action may include, but not be limited to, requiring a return of the grant from the charitable organization or requiring that donors make an additional non-deductible contribution.

Variance Power

If, at any time, the designated charities or charitable programs that the donor recommends for grants, become obsolete, go out of business, become suspect of wrongdoing (i.e. terrorist activities), are or become highly controversial, or otherwise significantly change in operation or mission, the Directors of The American Foundation may redirect the grant to other qualifying charities. The Directors of The American Foundation will first look to the donor and/or the component foundation’s Charitable Advisor for their recommendations and direction for any such needed substitution or modification of charity selection. In policy and practice, we favor donor charitable involvement and direction. This Variance Power is intended to protect and benefit the donor,The American Foundation and society. The American Foundation believes that donor direction results in more effective philanthropy, which is part of our primary charitable mission. Under this Variance Power, donors may lose their right of charitable direction only if their actions and grant making selections are intentionally harmful to society (such as making grants to support terrorist activities) or if they otherwise become contentious.

Minimum Charitable Grant Activity

It is the policy of The American Foundation that all family foundations make annual grants of 5% of the value of the foundation account principal (determined on January 1st of each year). This policy may be modified only when there are clear and reasonable reasons for doing so. Requests for grants may be made at any time, and should be made no later than December 1st of each year to qualify for the current calendar year.

If this requirement is not met in a year, The American Foundation will contact donors who have not had grant activity in their family foundation of at least 5% of the foundation account’s average net assets and provide them with the opportunity to recommend grants for the requisite amount. If such donors do not provide recommendations within 60 days after such notice, The American Foundation will make every effort to honor the wishes of the donor(s) by making the 5% annual grant in keeping with the respective donor’s Charitable Interest Mission Statement, if provided. If no written instructions are available, The American Foundation will make the 5% annual grant based on past grants. If this is not possible, then The American Foundation will use its best judgment to make grants to worthwhile charitable organizations and programs.

Grant Checks and Confirmations

Grants to charities are made by The American Foundation for Charitable Support accompanied by a letter recognizing the family foundation name and the name of the donor recommending the grant, unless anonymity is specifically requested. After your recommended grant is made, you will receive a written confirmation from The American Foundation.

Gift Allocation to The American Foundation

Helping us Fulfill our Mission

All foundation accounts transfer 1% of their foundation or trust account values annually to The American Foundation as a gift allocation.

Anyone making a gift to a family foundation account at The American Foundation™ establishes a donor/charity relationship with The American Foundation. The relationship is not one of fees for services.

The donation allocation to The American Foundation first pays for the actual costs of program administration. Remaining money is used to develop and expand our charitable mission.

We encourage those who believe in our charitable mission to allocate more than the minimum percentage to The American Foundation to help achieve our charitable objectives. In any event, all family foundations transfer a minimum annual gift allocation to The American Foundation of an amount equal to 1% of the foundation value.

The Perpetual Nature of Family Foundations

All of our family foundations are intended to operate as perpetual charitable accounts under The American Foundation’s Donor Advised Family Foundation Program. We endorse and promote the concept of preserving principal and try to manage all accounts to achieve growth. We feel the perpetual family foundation is a more effective and successful way to financially benefit charities and charitable programs. Giving to charity also becomes a more meaningful family endeavor.

Definition of Principal

Principal is the initial contribution plus any subsequent contributions. Any amounts of growth or income not distributed can be reclassified as principal. Growth and income are not guaranteed and we cannot guarantee against losses in investments which might diminish a donor’s contribution amount or principal. However it is our hope and expectation that we will always be able to achieve above average income and/or growth.

Donor Direction

If The American Foundation should change its declared and documented mission regarding its policy of allowing donors the ability to retain charitable direction (defined as the donor’s ability to be involved in the recommendations of grants to charities), we will be happy to transfer their family foundation to another of our charities that does allow for that mission or to one or more of the “operating charities” to which the donor’s family foundation has given grants. Operating charities are defined as charities that have charitable operating programs such as youth organizations, educational institutions, health organizations, churches, schools, etc. This “change of mission” policy is a donor friendly Donor Advised Family Foundation Program feature.

Always Seek Assistance

The American Foundation strongly recommends that individuals seek assistance from a qualified legal, financial, tax or other professional to review and determine the tax and legal issues regarding donations to the Donor Advised Family Foundation Program.

Charitable Deduction

Contributions made to a family foundation established with The American Foundation are deductible at the highest “public charity” level. You will be eligible to take an itemized deduction for a charitable contribution to a public charity on the date that the contribution is made to your family foundation, subject to the following general limitations. Your deduction will in part depend on the type of asset contributed to The American Foundation. You are encouraged to consult your legal or tax advisor to review your personal situation.

Cash

A cash contribution to your family foundation qualifies for a full income tax deduction (up to 50% of adjusted gross income).

Publicly Traded Securities

For publicly traded securities held for more than one year, your deduction is determined by the mean of the high and low prices reported on the date the contribution is made to your family foundation account. For mutual fund shares held for more than one year, your deduction is determined by the closing price on the date the contribution is made. For securities or mutual fund shares held for one year or less, the deduction is for the lesser of your cost basis or fair market value.

Securities That Are Not Publicly Traded

For securities that are not publicly traded which have been held for more than one year, the donor determines the fair market value in a reasonable manner on the date the contribution is made to the family foundation. To that end, the donor will be required to provide the IRS with a qualified appraisal for any contributed property for which the donor will claim a deduction of more than $5,000. For securities held for one year or less, the deduction is for the lesser of the cost basis or fair market value.

Other Deduction Limitations

Individual donors are eligible for an itemized deduction for cash contributions to your family foundation account in an amount up to 50% of their adjusted gross income in the tax year in which the contribution is made. Deductions for contributions of appreciated securities held for more than one year are limited to 30% of AGI. Any excess amount may be carried forward and deducted in the five-year period after the year of contribution. A donor’s ability to deduct itemized deductions may be subject to certain other limitations. Please contact your tax advisor to determine tax deductibility limits.

Estate Planning and Probate

Contributions to your family foundation and any earnings related to them are not part of your taxable estate and are not subject to probate. Amounts contributed to your family foundation should not be included in your gift and estate tax calculation.

Tax Treatment of The American Foundation’s Income Grants Made to Charitable Organizations

Income that accrues to your family foundation is income to your family foundation. It is not income to you, the donor(s), and is not available as a charitable deduction. Income to The American Foundation will be reflected in the value of the family foundation account.

Tax Treatment of Grants Made to Charitable Organizations

When The American Foundation makes grants from family foundations to qualified charitable organizations, The American Foundation is distributing its own assets. Donor(s) will not be eligible to claim additional charitable deductions in the amount of these grants. The amount distributed may include appreciation in the value of the family foundation since the date of contribution.

Record Keeping and Foundation Reporting

The American Foundation will provide donors with financial reports and other information as required by applicable law. The American Foundation will send the donor a funding letter and sign the “Donee Acknowledgment” at the bottom of IRS Form 8283 (when a gift requires an appraisal). The IRS requires that Form 8283 be completed and filed with an individual’s federal income tax return for gifts of property valued at $500 or more, or publicly traded securities valued at $5,000 or more.

Miscellaneous

The American Foundation

The American Foundation is a 501(c)(3) public charity as described in Sections 501(c)(3), 509(a)(1) and 170(b)(1)(A)(vi) of the Internal Revenue Code of 1986, as amended. The procedures and policies covered in this Program Description apply to all gifts made to The American Foundation, The American Foundation for Charitable Support, Inc., and all other affiliated foundations.

Changes to the Donor Advised Family Foundation Program

All activities of The American Foundation and donor participation in its Donor Advised Family Foundation Program, are subject to the terms and conditions of The American Foundation’s By-laws (“By-laws”) and the policies and procedures of this Donor Advised Family Foundation Program Description (“Description”) as published or found on its Internet Website, www.americanfoundation.org. The American Foundation Directors reserve the right to modify the Donor Advised Family Foundation Program under its full and total discretion, at any time, subject only to its allegiance to the policy of encouraging and allowing donor participation in making recommendations for charitable grants from their corresponding family foundation accounts. Any changes to the policies and procedures of the Donor Advised Family Foundation Program will be found in the Donor Advised Family Foundation Program as published on The American Foundation Website. A printed copy of the latest version of the Donor Advised Family Foundation Program can also be requested and mailed to donors or prospective donors by calling the Foundation offices.

Conflict of Terms

In the event of any inconsistency between the policies and procedures of this Plan Description and the By-laws, the terms of the By-laws will govern the rights and obligations of The American Foundation and donors.

Please Note

The information on this Site is not legal or financial advice, nor is it intended to be.

Since each individual’s circumstances will vary, The American Foundation strongly urges individuals to seek advice from qualified legal, financial, tax or other professionals when pursuing ideas presented on this Site.

FUNDING GUIDELINES

Below we have provided basic instructions for contributing cash, mutual funds, or securities to The American Foundation™. If you do not find instructions for your contribution type, or if you need assistance, please call The American Foundation at (602) 955-4770.

If you currently have a family foundation with The American Foundation and wish to make an additional contribution, please follow the instructions below, and fill out a copy of the “Additional Contribution” form. The American Foundation will confirm to you in writing the receipt of all assets.

| Mail to: |

The American Foundation™

4518 N. 32nd Street

Phoenix, AZ 85018

To establish a family foundation or to add to a family foundation, call:

Main Phone: (602) 955-4770

Fax: (602) 955-4707

Other important information:

Tax Status: 501(c)(3) Public Charity

Tax ID #: 86-0857725

Contribution Type: Mail/Fax to The American Foundation: Instructions:

CASH

| Check | Application and copy of check | Please make checks payable to “The American Foundation for Charitable Support.” Mail or deliver to broker for deposit to established foundation brokerage account.* |

| Wire Cash | Application | Please contact your investment advisor or broker (or call us) for the proper instructions to wire funds into your family foundation. |

STOCK CERTIFICATES

| Stock Certificates | Application and copy of endorsed certificate (we suggest using a mail method requiring a receipt) | Your investment advisor or broker (or call us if you do not have one) can instruct you on how to endorse certificates over to your newly established family foundation account. Date and sign the certificate exactly as your name appears on the front. Also, write the newly established foundation brokerage account number on the front, top-right corner of the certificate. Mail or deliver the certificates to your broker if an account has already been established or to The American Foundation if the account has not been established. |

CASH OR SECURITIES HELD AT FINANCIAL INVESTMENT FIRMS

| Securities and/or Mutual Funds Held at a Financial Institution | Application and a copy of the Letter of Instruction A | Submit original Letter of Instruction (see “Letter of Instruction A”) to the firm currently holding the securities. Instructions should request that shares are transferred directly to The American Foundation account name and number listed with your broker (see your broker or call us for the appropriate DTC #). |

| Mutual Funds Held at a Mutual Fund Company | Application and copy of the Letter of Instruction B |

Submit original Letter of Instruction (see “Letter of Instruction B”) to the mutual fund company. Instructions should request that shares are transferred directly to The American Foundation account name and number listed with your broker (see your broker or call us for the appropriate DTC #). Check with the fund company regarding signature guarantee requirements.

OTHER ASSETS

| Real Estate, Partnerships, Closely Held or Restricted Stock, Artwork or Other Assets | Application | Please contact The American Foundation before making any contribution of these types. The American Foundation™ will work with you or your financial and tax professionals to effectuate the transfer. The American Foundation will provide simple instructions that pertain to the asset in question and will authorize in writing the final transfer. |

* All contributions will be deposited into the donor’s family foundation at The American Foundation for Charitable Suppo